Launch this notebook on on mybinder.org:

Density estimation with sparse transport maps#

In this example we demonstrate how MParT can be use to build map with certain sparse structure in order to characterize high dimensional densities with conditional independence.

Imports#

First, import MParT and other packages used in this notebook. Note that it is possible to specify the number of threads used by MParT by setting the KOKKOS_NUM_THREADS environment variable before importing MParT.

[1]:

import numpy as np

from scipy.optimize import minimize

import matplotlib.pyplot as plt

from scipy.stats import multivariate_normal

from tqdm import tqdm

import os

os.environ['KOKKOS_NUM_THREADS'] = '8'

import mpart as mt

print('Kokkos is using', mt.Concurrency(), 'threads')

plt.rcParams['figure.dpi'] = 110

Kokkos::OpenMP::initialize WARNING: You are likely oversubscribing your CPU cores.

process threads available : 4, requested thread : 8

Kokkos::OpenMP::initialize WARNING: You are likely oversubscribing your CPU cores.

Detected: 4 cores per node.

Detected: 1 MPI_ranks per node.

Requested: 8 threads per process.

Kokkos is using 8 threads

Stochastic volatility model#

Problem description#

The problem considered here is a Markov process that describes the volatility on a financial asset overt time. The model depends on two hyperparamters \(\mu\) and \(\phi\) and state variable \(Z_k\) represents log-volatility at times \(k=1,...,T\). The log-volatility follows the order-one autoregressive process:

where

The objective is to characterize the joint density of

with \(T\) being arbitrarly large.

The conditional independence property for this problem reads

More details about this problem can be found in [Baptista et al., 2022].

Sampling#

Drawing samples \((\mu^i,\phi^i,x_0^i,x_1^i,...,x_T^i)\) can be performed by the following function

[2]:

def generate_SV_samples(d,N):

# Sample hyper-parameters

sigma = 0.25

mu = np.random.randn(1,N)

phis = 3+np.random.randn(1,N)

phi = 2*np.exp(phis)/(1+np.exp(phis))-1

X = np.vstack((mu,phi))

if d > 2:

# Sample Z0

Z = np.sqrt(1/(1-phi**2))*np.random.randn(1,N) + mu

# Sample auto-regressively

for i in range(d-3):

Zi = mu + phi * (Z[-1,:] - mu)+sigma*np.random.randn(1,N)

Z = np.vstack((Z,Zi))

X = np.vstack((X,Z))

return X

Set dimension of the problem:

[3]:

T = 30 #number of time steps including initial condition

d = T+2

Few realizations of the process look like

[4]:

Nvisu = 10 #Number of samples

Xvisu = generate_SV_samples(d, Nvisu)

Zvisu = Xvisu[2:,:]

plt.figure()

plt.plot(Zvisu)

plt.xlabel("Days (d)")

plt.show()

And corresponding realization of hyperparameters

[5]:

hyper_params = Xvisu[:2,:]

plt.figure()

plt.plot(range(1,Nvisu+1),Xvisu[1,:],label='$\mu$')

plt.plot(range(1,Nvisu+1),Xvisu[2,:],label='$\phi$')

plt.xlabel('Samples')

plt.legend()

plt.show()

<>:3: SyntaxWarning: invalid escape sequence '\m'

<>:4: SyntaxWarning: invalid escape sequence '\p'

<>:3: SyntaxWarning: invalid escape sequence '\m'

<>:4: SyntaxWarning: invalid escape sequence '\p'

/tmp/ipykernel_268/2191412704.py:3: SyntaxWarning: invalid escape sequence '\m'

plt.plot(range(1,Nvisu+1),Xvisu[1,:],label='$\mu$')

/tmp/ipykernel_268/2191412704.py:4: SyntaxWarning: invalid escape sequence '\p'

plt.plot(range(1,Nvisu+1),Xvisu[2,:],label='$\phi$')

Probability density function#

The exact log-conditional densities used to define joint density \(\pi(\mathbf{x}_T)\) are defined by the following function:

[6]:

def SV_log_pdf(X):

def normpdf(x,mu,sigma):

return np.exp(-0.5 * ((x - mu)/sigma)**2) / (np.sqrt(2*np.pi) * sigma)

sigma = 0.25

# Extract variables mu, phi and states

mu = X[0,:]

phi = X[1,:]

Z = X[2:,:]

# Compute density for mu

piMu = multivariate_normal(np.zeros(1),np.eye(1))

logPdfMu = piMu.logpdf(mu)

# Compute density for phi

phiRef = np.log((1+phi)/(1-phi))

dphiRef = 2/(1-phi**2)

piPhi = multivariate_normal(3*np.ones(1),np.eye(1))

logPdfPhi = piPhi.logpdf(phiRef)+np.log(dphiRef)

# Add piMu, piPhi to density

logPdf = np.vstack((logPdfMu,logPdfPhi))

# Number of time steps

dz = Z.shape[0]

if dz > 0:

# Conditonal density for Z_0

muZ0 = mu

stdZ0 = np.sqrt(1/(1-phi**2))

logPdfZ0 = np.log(normpdf(Z[0,:],muZ0,stdZ0))

logPdf = np.vstack((logPdf,logPdfZ0))

# Compute auto-regressive conditional densities for Z_i|Z_{1:i-1}

for i in range(1,dz):

meanZi = mu + phi * (Z[i-1,:]-mu)

stdZi = sigma

logPdfZi = np.log(normpdf(Z[i,:],meanZi,stdZi))

logPdf = np.vstack((logPdf,logPdfZi))

return logPdf

Transport map training#

In the following we optimize each map component \(S_k\), \(k \in \{1,...,T+2\}\):

For \(k=1\), map \(S_1\) characterize marginal density \(\pi(\mu)\)

For \(k=2\), map \(S_2\) characterize conditional density \(\pi(\phi|\mu)\)

For \(k=3\), map \(S_3\) characterize conditional density \(\pi(z_0|\phi,\mu)\)

For \(k>3\), map \(S_k\) characterize conditional density \(\pi(z_{k-2}|z_{k-3},\phi,\mu)\)

Definition of log-conditional density from map component \(S_k\)

[7]:

def log_cond_pullback_pdf(triMap,eta,x):

r = triMap.Evaluate(x)

log_pdf = eta.logpdf(r.T)+triMap.LogDeterminant(x)

return log_pdf

Generating training and testing samples#

From training samples generated with the known function we compare accuracy of the transport map induced density using different parameterization and a limited number of training samples.

[8]:

N = 2000 #Number of training samples

X = generate_SV_samples(d, N)

Ntest = 5000 # Number of testing samples

Xtest = generate_SV_samples(d,Ntest)

Objective function and gradient#

We use the minimization of negative log-likelihood to optimize map components.

For map component \(k\), the objective function is given by

and corresponding gradient

[9]:

### Negative log likelihood objective

def obj(coeffs, tri_map,x):

""" Evaluates the log-likelihood of the samples using the map-induced density. """

num_points = x.shape[1]

tri_map.SetCoeffs(coeffs)

# Compute the map-induced density at each point

map_of_x = tri_map.Evaluate(x)

rho = multivariate_normal(np.zeros(tri_map.outputDim),np.eye(tri_map.outputDim))

rho_of_map_of_x = rho.logpdf(map_of_x.T)

log_det = tri_map.LogDeterminant(x)

# Return the negative log-likelihood of the entire dataset

return -np.sum(rho_of_map_of_x + log_det)/num_points

def grad_obj(coeffs, tri_map, x):

""" Returns the gradient of the log-likelihood objective wrt the map parameters. """

num_points = x.shape[1]

tri_map.SetCoeffs(coeffs)

# Evaluate the map

map_of_x = tri_map.Evaluate(x)

# Now compute the inner product of the map jacobian (\nabla_w S) and the gradient (which is just -S(x) here)

grad_rho_of_map_of_x = -tri_map.CoeffGrad(x, map_of_x)

# Get the gradient of the log determinant with respect to the map coefficients

grad_log_det = tri_map.LogDeterminantCoeffGrad(x)

return -np.sum(grad_rho_of_map_of_x + grad_log_det, 1)/num_points

Training total order 1 map#

Here we use a total order 1 multivariate expansion to parameterize each component \(S_k\), \(k \in \{1,...,T+2\}\).

[10]:

opts = mt.MapOptions()

opts.basisType = mt.BasisTypes.HermiteFunctions

Optimization#

[11]:

# Total order 1 approximation

totalOrder = 1

logPdfTM_to1 = np.zeros((d,Ntest))

ListCoeffs_to1=np.zeros((d,))

for dk in tqdm(range(1,d+1),desc="Map component"):

fixed_mset= mt.FixedMultiIndexSet(dk,totalOrder)

S = mt.CreateComponent(fixed_mset,opts)

Xtrain = X[:dk,:]

Xtestk = Xtest[:dk,:]

ListCoeffs_to1[dk-1]=S.numCoeffs

options={'gtol': 1e-3, 'disp': False}

res = minimize(obj, S.CoeffMap(), args=(S, Xtrain), jac=grad_obj, method='BFGS', options=options)

# Reference density

eta = multivariate_normal(np.zeros(S.outputDim),np.eye(S.outputDim))

# Compute log-conditional density at testing samples

logPdfTM_to1[dk-1,:]=log_cond_pullback_pdf(S,eta,Xtestk)

Map component: 100%|██████████| 32/32 [00:02<00:00, 11.61it/s]

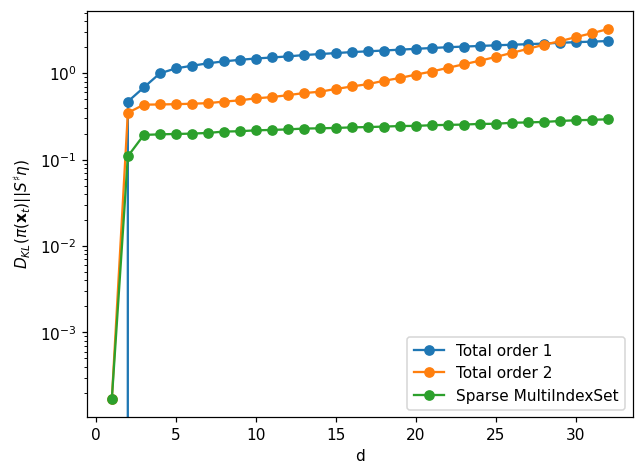

Compute KL divergence error#

Since we know what the true is for problem we can compute the KL divergence \(D_{KL}(\pi(\mathbf{x}_t)||S^\sharp \eta)\) between the map-induced density and the true density.

[12]:

logPdfSV = SV_log_pdf(Xtest) # true log-pdf

def compute_joint_KL(logPdfSV,logPdfTM):

KL = np.zeros((logPdfSV.shape[0],))

for k in range(1,d+1):

KL[k-1]=np.mean(np.sum(logPdfSV[:k,:],0)-np.sum(logPdfTM[:k,:],0))

return KL

# Compute joint KL divergence for total order 1 approximation

KL_to1 = compute_joint_KL(logPdfSV,logPdfTM_to1)

Training total order 2 map#

Here we use a total order 2 multivariate expansion to parameterize each component \(S_k\), \(k \in \{1,...,T+2\}\).

Optimization#

This step can take few minutes depending on the number of time steps set at the definition of the problem.

[13]:

# Total order 2 approximation

totalOrder = 2

logPdfTM_to2 = np.zeros((d,Ntest))

ListCoeffs_to2=np.zeros((d,))

for dk in tqdm(range(1,d+1),desc="Map component"):

fixed_mset= mt.FixedMultiIndexSet(dk,totalOrder)

S = mt.CreateComponent(fixed_mset,opts)

Xtrain = X[:dk,:]

Xtestk = Xtest[:dk,:]

ListCoeffs_to2[dk-1]=S.numCoeffs

options={'gtol': 1e-3, 'disp': False}

res = minimize(obj, S.CoeffMap(), args=(S, Xtrain), jac=grad_obj, method='BFGS', options=options)

# Reference density

eta = multivariate_normal(np.zeros(S.outputDim),np.eye(S.outputDim))

# Compute log-conditional density at testing samples

logPdfTM_to2[dk-1,:]=log_cond_pullback_pdf(S,eta,Xtestk)

Map component: 100%|██████████| 32/32 [05:41<00:00, 10.67s/it]

Compute KL divergence error#

[14]:

# Compute joint KL divergence for total order 2 approximation

KL_to2 = compute_joint_KL(logPdfSV,logPdfTM_to2)

Training sparse map#

Here we use the prior knowledge of the conditional independence property of the target density \(\pi(\mathbf{x}_T)\) to parameterize map components with a map structure.

Prior knowledge used to parameterize map components#

From the independence structure mentionned in the problem formulation we have:

\(\pi(\mu,\phi)=\pi(\mu)\pi(\phi)\), meaning \(S_2\) only dependes on \(\phi\)

\(\pi(z_{k-2}|z_{k-3},...,z_{0},\phi,\mu)=\pi(z_{k-2}|z_{k-3},\phi,\mu),\,\, k>3\), meaning \(S_k\), only depends on \(z_{k-2}\),\(z_{k-3}\), \(\phi\) and \(\mu\)

Complexity of map component can also be deducted from problem formulation:

\(\pi(\mu)\) being a normal distribution, \(S_1\) should be of order 1.

\(\pi(\phi)\) is non-Gaussian such that \(S_2\) should be nonlinear.

\(\pi(z_{k-2}|z_{k-3},\phi,\mu)\) can be represented by a total order 2 parameterization due to the linear autoregressive model.

Hence multi-index sets used for this problem are:

\(k=1\): 1D expansion of order \(\geq\) 1

\(k=2\): 1D expansion (depending on last component) of high order \(>1\)

\(k=3\): 3D expansion of total order 2

\(k>3\): 4D expansion (depending on first two and last two components) of total order 2

Optimization#

[15]:

totalOrder = 2

logPdfTM_sa = np.zeros((d,Ntest))

ListCoeffs_sa = np.zeros((d,))

# MultiIndexSet for map S_k, k>3

mset_to= mt.MultiIndexSet.CreateTotalOrder(4,totalOrder,mt.NoneLim())

maxOrder=9 # order for map S_2

for dk in tqdm(range(1,d+1),desc="Map component"):

if dk == 1:

fixed_mset= mt.FixedMultiIndexSet(1,totalOrder)

S = mt.CreateComponent(fixed_mset,opts)

Xtrain = X[dk-1,:].reshape(1,-1)

Xtestk = Xtest[dk-1,:].reshape(1,-1)

elif dk == 2:

fixed_mset= mt.FixedMultiIndexSet(1,maxOrder)

S = mt.CreateComponent(fixed_mset,opts)

Xtrain = X[dk-1,:].reshape(1,-1)

Xtestk = Xtest[dk-1,:].reshape(1,-1)

elif dk==3:

fixed_mset= mt.FixedMultiIndexSet(dk,totalOrder)

S = mt.CreateComponent(fixed_mset,opts)

Xtrain = X[:dk,:]

Xtestk = Xtest[:dk,:]

else:

multis=np.zeros((mset_to.Size(),dk))

for s in range(mset_to.Size()):

multis_to = np.array([mset_to[s].tolist()])

multis[s,:2]=multis_to[0,:2]

multis[s,-2:]=multis_to[0,-2:]

mset = mt.MultiIndexSet(multis)

fixed_mset = mset.fix(True)

S = mt.CreateComponent(fixed_mset,opts)

Xtrain = X[:dk,:]

Xtestk = Xtest[:dk,:]

ListCoeffs_sa[dk-1]=S.numCoeffs

options={'gtol': 1e-3, 'disp': False}

res = minimize(obj, S.CoeffMap(), args=(S, Xtrain), jac=grad_obj, method='BFGS', options=options)

rho = multivariate_normal(np.zeros(S.outputDim),np.eye(S.outputDim))

logPdfTM_sa[dk-1,:]=log_cond_pullback_pdf(S,rho,Xtestk)

Map component: 100%|██████████| 32/32 [00:15<00:00, 2.08it/s]

Compute KL divergence error#

[16]:

# Compute joint KL divergence

KL_sa = compute_joint_KL(logPdfSV,logPdfTM_sa)

Compare approximations#

KL divergence#

[17]:

# Compare map approximations

fig, ax = plt.subplots()

ax.plot(range(1,d+1),KL_to1,'-o',label='Total order 1')

ax.plot(range(1,d+1),KL_to2,'-o',label='Total order 2')

ax.plot(range(1,d+1),KL_sa,'-o',label='Sparse MultiIndexSet')

ax.set_yscale('log')

ax.set_xlabel('d')

ax.set_ylabel('$D_{KL}(\pi(\mathbf{x}_t)||S^\sharp \eta)$')

plt.legend()

plt.show()

<>:8: SyntaxWarning: invalid escape sequence '\p'

<>:8: SyntaxWarning: invalid escape sequence '\p'

/tmp/ipykernel_268/1071692651.py:8: SyntaxWarning: invalid escape sequence '\p'

ax.set_ylabel('$D_{KL}(\pi(\mathbf{x}_t)||S^\sharp \eta)$')

Usually increasing map complexity will improve map approximation. However when the number of parameters increases too much compared to the number of samples, computed map overfits the data which lead to worst approximation. This overfitting can be seen in this examples when looking at the total order 2 approximation that rapidly loses accuracy when the dimension increases.

Using sparse multi-index sets help reduces the increase of parameters when the dimension increases leading to better approximation for all dimensions.

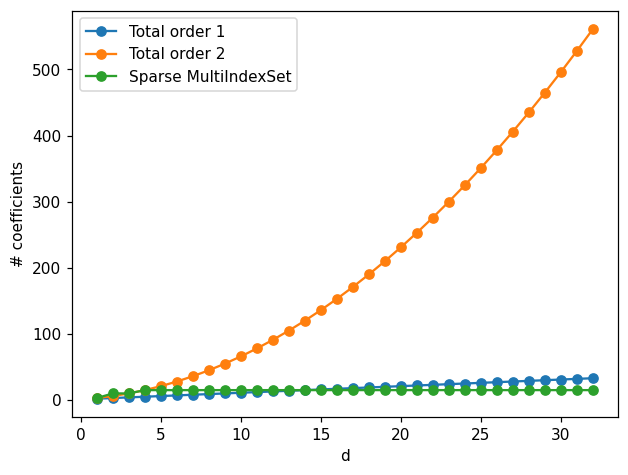

Map coefficients#

To complement observations made above, we visualize the number of parameters (polyniomal coefficients) for each map parameterization.

[18]:

fig, ax =plt.subplots()

ax.plot(range(1,d+1),ListCoeffs_to1,'-o',label='Total order 1')

ax.plot(range(1,d+1),ListCoeffs_to2,'-o',label='Total order 2')

ax.plot(range(1,d+1),ListCoeffs_sa,'-o',label='Sparse MultiIndexSet')

ax.set_xlabel('d')

ax.set_ylabel('# coefficients')

plt.legend()

plt.show()

We can observe the exponential growth of the number coefficients for the total order 2 approximation. Chosen sparse multi-index sets have a fixed number of parameters which become smaller than the number of parameters of the total order 1 approximation when dimension is 15.

Using less parameters helps error scaling with dimension but aslo helps reducing computation time for the optimization and the evaluation the transport maps.